$18.8 Trillion in Debt. $34.1 Trillion in Home Equity. Most Americans Have Never Seen Both Numbers Together.

Most people know roughly what they owe.

Almost nobody knows, in specific dollar terms, what they own.

Those two facts sitting next to each other are the most underreported financial story of 2026.

What Americans Owe

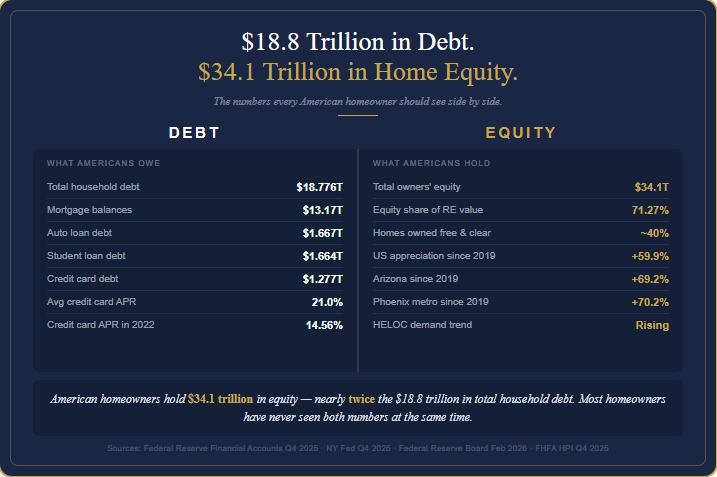

Total household debt in the United States reached $18.776 trillion in Q4 2025, a nominal all-time high according to the Federal Reserve Bank of New York. Credit cards, auto loans, and student loans combined total approximately $4.6 trillion of that figure.

Credit card rates stand at 21.0 percent as of February 2026, up from 14.56 percent in February 2022. That is a 6.4 percentage point increase over four years. The same balance costs more to hold today than it did in 2022. A household carrying $15,000 at today’s rate pays $966 more per year in interest than it did four years ago on the exact same balance.

Source: NY Fed Q4 2025 · Federal Reserve Board G.19 February 2026

[ READ MORE — Full breakdown of American household debt → ]

What American Homeowners Hold

The Federal Reserve’s Q4 2025 financial accounts put total owners’ equity in real estate at $34.1 trillion. Owner-occupied real estate is valued at $47.9 trillion. Homeowners own 71.27 percent of that value outright. Approximately 40 percent of owner-occupied homes carry no mortgage at all.

National home prices are up 59.9 percent since Q4 2019 according to the FHFA all-transactions index. In Arizona the numbers are stronger. Phoenix metro up 70.2 percent. Flagstaff up 79 percent. A home purchased in Phoenix for $300,000 at the end of 2019 is worth approximately $511,000 today based on that index.

Source: Federal Reserve Financial Accounts Q4 2025 · FHFA HPI Q4 2025

[ READ MORE — Full breakdown of American home equity → ]

What Happens When You Put Both Numbers on the Same Page

Consumer debt, credit cards, auto loans, and student loans, totals approximately $4.6 trillion. Home equity is $34.1 trillion. The asset is more than seven times larger than the consumer debt.

Even comparing total household debt against total home equity, $18.776 trillion against $34.1 trillion, homeowners hold nearly twice as much in equity as they owe across all forms of debt combined.

$4.6 trillion in consumer debt at 21 percent interest. $34.1 trillion in home equity. The asset is seven times larger than the liability. Most homeowners have never seen those two numbers at the same time.

The Federal Reserve’s April 2026 Senior Loan Officer Opinion Survey found HELOC demand strengthening while demand for credit cards and auto loans was weakening. HELOC balances grew $11.6 billion in Q4 2025 alone. That expansion has been running since 2022.

2022 is the same year credit card rates started climbing.

Some homeowners are already looking at both sides of their balance sheet. Most are not. Because most have never seen both numbers at the same time.

Until now.

Source: Federal Reserve April 2026 SLOOS · NY Fed Q4 2025