Credit Card Rates Are at a 20-Year High. Here Is What the Federal Reserve Data Shows.

In February 2022, the average American credit card rate was 14.56 percent.

By February 2026 it was 21 percent.

The balance did not change. The cost of carrying it did.

That shift happened quietly. No announcement. No letter explaining that the interest on your existing balance just became significantly more expensive. The Federal Reserve raised its benchmark rate to fight inflation. Credit card rates are variable. They moved in lockstep. The minimum payment adjusted. Life continued.

Most people never stopped to calculate what that actually cost them on the balance they were already carrying.

These numbers did.

The Rate History the Fed Actually Recorded

The Federal Reserve Board publishes a monthly series tracking credit card rates across all accounts. Here is what that series shows:

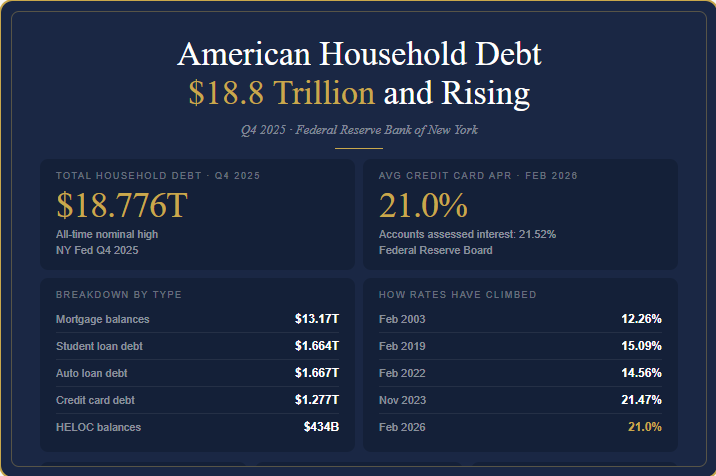

February 2003: 12.26 percent

February 2019: 15.09 percent

February 2022: 14.56 percent

February 2023: 20.09 percent

November 2023: 21.47 percent

February 2026: 21.0 percent (all accounts)

February 2026: 21.52 percent (accounts being charged interest)

For most of the 2000s and 2010s, the average American credit card rate sat in the low to mid teens. That was the environment most households built their budgets around.

Between February 2022 and February 2023, a period of twelve months, the rate moved from 14.56 percent to 20.09 percent. That is a 5.5 percentage point increase in a single year.

What does that mean for a real household? A balance of $15,000 at 14.56 percent costs $2,184 per year in interest. At 21 percent, that same balance costs $3,150 per year. The balance is identical. The annual cost is $966 higher. That $966 does not reduce what is owed. It goes entirely to the cost of holding the debt.

The same $15,000 balance costs $966 more per year today than it did in 2022. The debt did not grow. The price of holding it did.

Source: Federal Reserve Board of Governors, Consumer Credit G.19, February 2026

What Total Household Debt Looks Like Right Now

The Federal Reserve Bank of New York’s Q4 2025 Household Debt and Credit Report puts total household debt at $18.776 trillion. That is a nominal all-time high.

Mortgage balances: $13.17 trillion

Auto loan debt: $1.667 trillion

Student loan debt: $1.664 trillion

Credit card debt: $1.277 trillion

HELOC balances: $434 billion

Mortgage balances make up the largest share and reflect the size of the housing market more than consumer spending. Consumer debt, credit cards, auto loans, and student loans combined, totals approximately $4.6 trillion.

How does that compare to the asset side of the ledger for homeowners? American home equity in Q4 2025 was $34.1 trillion. The asset is more than seven times the size of the consumer debt. Most people have never seen both numbers at the same time.

Source: Federal Reserve Bank of New York, Household Debt and Credit Report, Q4 2025

Is This Level of Debt a Crisis?

The raw dollar total is a nominal all-time high. But the Federal Reserve tracks a more precise measure: the ratio of household debt to disposable personal income.

By that measure the picture is more nuanced. The debt-to-income ratio stood at 0.90 in Q4 2025, near its lowest level since the late 1990s. The household debt-service ratio, required payments as a share of income, was 11.32 percent. That is below the 11.73 percent of late 2019 and far below the 15.85 percent peak of late 2007.

The Fed’s own financial stability report in late 2025 described the household debt-to-GDP ratio as being at more than 20-year lows. Mortgage credit risk was described as low. The balances are large. The burden relative to income, for most households, is not at crisis levels.

The stress is real. It is not evenly distributed.

Source: Federal Reserve Financial Accounts of the United States, Q4 2025

Where the Stress Is Showing Up

The New York Fed reported in Q4 2025 that transitions into serious delinquency increased across credit cards, mortgages, and student loans simultaneously.

Student loan delinquency is the most striking data point. After the pandemic-era pause on payment reporting ended, 9.6 percent of student loan balances were 90 or more days past due. Approximately one million borrowers more than 120 days past due had their loans transferred to the Education Department’s Default Resolution Group.

On mortgages, the Mortgage Bankers Association reported 4.26 percent of loans were delinquent at the end of Q4 2025. Foreclosure filings in Q1 2026 were up 26 percent compared to Q1 2025 nationally, according to ATTOM Data Solutions. That number is real. The context that rarely follows it: filings are still 25 percent below 2019 levels and 87 percent below the 2010 peak. In Arizona specifically, foreclosure filings in Q1 2026 were up 31 percent from a year earlier in the same tracker.

The Fed noted that mortgage delinquency deterioration is concentrated in lower-income areas and markets where home prices have softened. It is not a generalized crisis. It is localized stress inside a market that still has unusually strong equity cushions.

Source: NY Fed Q4 2025 · Mortgage Bankers Association Q4 2025 · ATTOM Q1 2026 Foreclosure Market Report

What Is Already Shifting

The Federal Reserve’s April 2026 Senior Loan Officer Opinion Survey found something that did not make many headlines. Demand for credit cards and auto loans was weakening. Demand for home equity lines of credit was strengthening.

HELOC balances grew by $11.6 billion in Q4 2025 alone, reaching $434 billion total. The New York Fed reported that this HELOC expansion has been running continuously since 2022.

2022 is the same year credit card rates started their sharpest climb in more than two decades.

Some homeowners are already connecting those two facts. They are looking at what they owe on one side and what their home is worth on the other.

Source: Federal Reserve April 2026 Senior Loan Officer Opinion Survey · NY Fed Q4 2025

Credit card rates at a 20-year high. Student loan delinquency at 9.6 percent. HELOC demand rising for three straight years.

The numbers do not need any interpretation. They are already telling the story.

One Response